Lyle Solomon

Lyle Solomon

Loretta Kilday

Loretta Kilday

Updated: • 18 min read

Kansas debt collection laws - Statute of limitations and how to get out of debt

- Before a lender can take your car or sue you, they usually must send a "Right to Cure" notice giving you 20 days to catch up.

- Collectors cannot leave you with nothing. You are guaranteed to keep at least $217.50 per week (based on current minimum wage laws), and often much more.

- If a credit card debt is more than 3 years old, the collector might not be able to sue you. But be careful, paying even $1 can restart the clock.

- Hospitals often have to follow specific charity care rules before sending you to collections.

- If you get court papers, you must file an "Answer." If you do nothing, they win automatically.

Many debt collectors use intimidation tactics to pressure consumers into paying. They want you to believe that they have all the power to take your home, your car or garnish your paycheck whenever they want.

However, Kansas law limits what collectors can actually do.

As a consumer, you are not powerless. In fact, Kansas debt collection laws are some of the strongest in the country. Kansas has its own legal shield called the 'Uniform Consumer Credit Code (UCCC)'. This law applies not just to scam debt collection agencies, but often to the original banks and creditors, too.

Here, you'll see exactly how to use the law to stop the collection calls, protect your paycheck, and fight back.

Debt collection actions permitted by law

Legal collection actions are normally started by letter or phone call, but the law also allows other means of contact, such as email, faxes, and even in person visits.

A debt collection agency is required to give proof of the debts they claim are owed after initial contact, including the full amount owed, the original creditor's name and other details.

Actions prohibited by debt collection laws in Kansas

Under Kansas debt collection laws, collectors are prohibited from:

- Contacting you after receiving a written request to stop, unless to report activities on a specific debt or inform you the debt has been discharged.

- Using obscene, harassing or threatening language when speaking with you.

- Threatening or implying legal action (such as liens or wage garnishments) unless they genuinely intend to follow through.

- Implying they are attorneys, government officials, or serving in any official capacity other than debt collectors.

If a debt collector breaks these rules, you can file a lawsuit in state or federal court. You must file the lawsuit within one year of the violation.

Make sure a debt collection service follows specific rules if you get a call, email, letter, or fax from them alleging you owe money. Some of them are as follows:

- They have to call between 8:00 am and 9:00 pm; they can't be rude, obscene, threatening, or otherwise intimidating.

- They must not call you at your place of employment if they are aware that your boss does not permit you to take personal calls.

- They must call your attorney instead of you if you let them know that you have one.

There may be grounds for debt harassment claims if any of these rules and a few others are broken. Consumers in Kansas who believe that they've become victims of debt harassment have a legal right to submit complaints to the Kansas Attorney General.

Federal vs. State Protection

To protect yourself, you need to know which protection you may use.

1. The Federal Shield (FDCPA)

The Fair Debt Collection Practices Act (FDCPA) is a federal law that stops third - party debt collectors from violating debt collection rules. As per the law, debt collectors can't:

- Call you at 2 AM.

- Threaten to arrest you.

- Lie about how much you owe.

2. The Kansas Legal Protection (UCCC & KCPA)

This is where debt collection laws in Kansas really shine.

The Uniform Consumer Credit Code (UCCC): This law (K.S.A. 16a) covers loans, credit cards, and car notes. It limits what original creditors can do - not just third - party collectors. It caps the interest they can charge and forces them to give consumers a statutory warning before taking legal action.

The Kansas Consumer Protection Act (KCPA): This law (K.S.A. 50 - 623) bans 'unfair' and 'deceptive' acts. If a collector tricks you, they aren't just breaking a rule; they might be breaking the law, and you could sue them for damages.

Federal vs. Kansas State Protection - At a Glance

| Protection Area | Federal (FDCPA) | Kansas State (UCCC & KCPA) |

|---|---|---|

| Who It Covers | Third party collectors only | Original creditors AND third party collectors |

| Calling Hours | 8 AM–9 PM | 8 AM–9 PM |

| Harassment Ban | Yes | Yes |

| Interest Rate Caps | No | Yes (UCCC caps rates) |

| Right to Cure Notice | Not required | Required (20 - day written warning) |

| Deceptive Practices | Prohibited | Prohibited (plus private right to sue under KCPA) |

| Damages for Violations | Up to $1,000 per violation | Actual damages plus potential penalties |

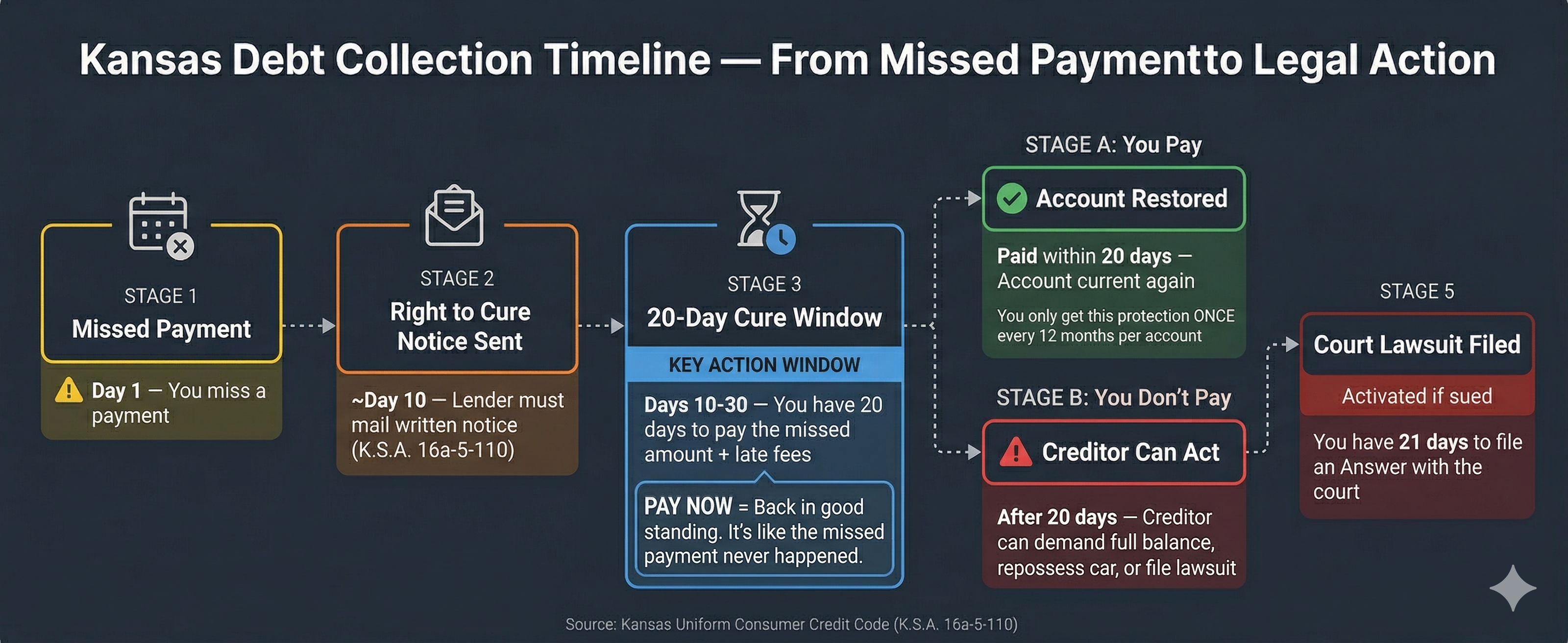

The Notice of Right to Cure - The 20 Day Warning

The Right to Cure notice is an important consumer protection in Kansas debt collection laws. It stops creditors from blindsiding you.

Under Kansas law (K.S.A. 16a - 5 - 110), a creditor generally cannot just demand the full balance of your loan or repossess your car the moment you miss a payment. They have to give you a chance to fix it first.

How It Works

- You miss a payment and are about 10 days late.

- The lender must send you a written 'Notice of Right to Cure Default.'

- You have 20 days from the date they mailed it to pay the missed amount (plus any late fees).

- If you pay that specific amount, you are back in good standing. It's like the missed payment never happened.

The 'One Strike' Rule

You have to remember that you usually only get this protection once every 12 months for the same account. If you fix it in February but miss a payment again in April, they might not have to send another letter before repossessing your vehicle.

Kansas statute of limitations on debt collection

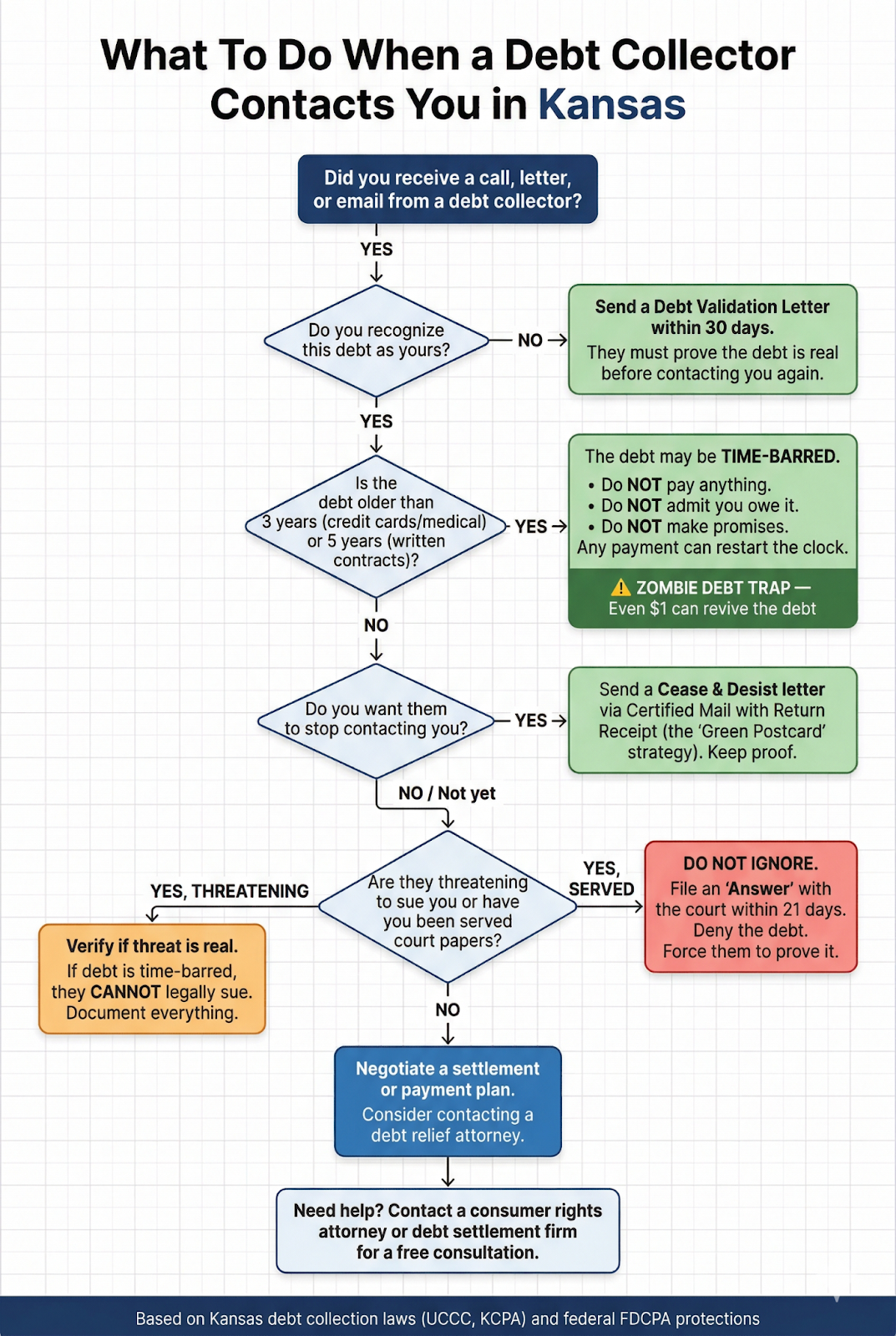

One of the biggest fears people have is being sued for a mistake they probably made 10 years ago. But the debt collection laws Kansas enforces include strict time limits for debts to be collected. This is called the Statute of Limitations - the legal deadline after which a creditor can no longer file a lawsuit to collect a debt.

Once a debt passes this time limit, it becomes 'time - barred.' The debt collector can still ask you to pay, but they cannot legally sue you to force you to pay.

| Type of Debt | Time Limit | Legal Source |

|---|---|---|

| Credit Cards (Open Accounts) | 3 Years | K.S.A. 60 - 512 |

| Medical Bills (Unwritten) | 3 Years | K.S.A. 60 - 512 |

| Written Contracts | 5 Years | K.S.A. 60 - 511 |

| Promissory Notes | 5 Years | K.S.A. 60 - 511 |

| Court Judgments | 5 Years | K.S.A. 60 - 2403 |

Many collectors will try to tell you that a credit card is a 'written contract' and has a 5 - year limit. However, many Kansas courts have ruled that credit cards are 'open - ended accounts,' which means the limit is only 3 years.

The 'Zombie Debt' & How To Handle It

Let's say you have an old debt from 6 years ago. It is legally dead, so you don't have to pay it. A debt collector might call you and say, 'Look, just pay us $20 today to show us you're trying. We'll leave you alone.' This is called a Zombie Debt Trap.

Jeffrey Zhou, CEO & Founder, Fig Loans, explained, 'Zombie debt collectors are not reliant upon loopholes for their survival. They rely on one single statement: 'I do recall that debt.'

The moment an individual admits to owing a debt which has passed its statute of limitations, or makes any type of payment, the statute of limitations is completely reset. Collectors know this; most consumers don't'.

What To Do:

- Do not pay it at all. If you pay even $1, or if you sign a paper that the debt is yours, you can 'revive' the SOL of that debt. As a result, a debt that you didn't have to pay will be fully collectible, and the debt collectors can sue you for the whole amount plus years of interest.

- If you are unsure how old a debt is, do not pay, do not promise to pay, and do not panic! Ask for a 'Debt Validation Letter' first.

Nick Heimlich, Owner and Attorney, Nick Heimlich Law, added - 'Kansas statutes limit how many times debt collectors can try to collect on an 'old' or 'zombie' debt. If the statute of limitations has run out, then the debt collector may not pursue legal action against you for the debt nor can they take money from your paycheck through wage garnishment to pay off the debt'.

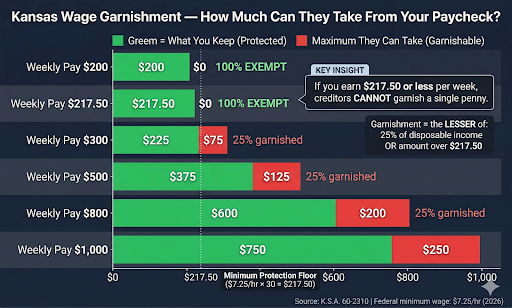

How To Protect Your Paycheck From Wage Garnishment In Kansas

If a collector sues you and wins, they can get a court order to take money directly from your paycheck. This is called 'wage garnishment' - a legal process where a portion of your earnings is withheld by your employer and sent to a creditor. But they cannot take it all. Kansas debt collection laws protect a portion of your income so you can still pay for necessities such as food and rent.

The Floor Calculation (2026)

Kansas uses a specific formula to figure out how much you get to keep. They cannot garnish your weekly earnings if they are less than 30 times the federal minimum wage.

- Federal Minimum Wage: $7.25/hr (as of early 2026).

- The Math: $7.25 × 30 = $217.50.

This Means:

- If you take home $215 a week, they cannot take a single penny. Your income is 100% exempt.

- If you take home more, they can usually take 25% of your disposable income, OR the amount that is over $217.50 - whichever is less.

Kansas Wage Garnishment Examples:

The garnishment amount is always the lesser of 25% of disposable income OR the amount over $217.50.

The Illness Exception

Under K.S.A. 60 - 2310, if illness kept you (or a family member) from working for two weeks or more, creditors cannot garnish your wages. This protection lasts until two months after you recover.

But, as per the law, you will need a doctor's note and may need to file an affidavit with the court.

Kansas Medical Debt Collection Laws

Medical debt is the most common reason Americans go bankrupt, and Kansas is no exception. When dealing with Kansas medical debt collection laws, you need to treat these bills differently from credit cards.

1. The No Surprises Factor

Federal law (the No Surprises Act) protects you from emergency room bills from out - of - network doctors. For example - If you went to an in - network hospital but got a bill from an out - of - network anesthesiologist, that bill might be illegal.

2. Financial Assistance Policies

Nonprofit hospitals in Kansas are required to have Financial Assistance Policies. Before they send you to collections, they are often required to check if you qualify for free or discounted care. These are some of the financial assistance policies in Kansas for medical care:

- Charity Care: Many hospitals have programs to help low-income patients pay their bills, even if the law doesn't say they have to.

- Medical Assistance: Some doctors or clinics charge different prices depending on how much money you make. This is often called a 'sliding scale.' You will need to show documents to prove your income.

- Charitable Health Care Provider Program: Doctors in this program agree to give free medical care to patients who earn very little money, usually below a specific poverty limit.

Before you pay a cent, call the hospital's billing department and ask about your eligibility to get medical financial assistance.

3. The 3 - Year statute of limitations

Unless you signed a specific promissory note with the hospital, Kansas medical debt collection laws often fall under the 3 - year statute of limitations for 'open accounts' or unwritten contracts under K.S.A. 60 - 512. If a collector is chasing you for a surgery from 2021, verify the dates carefully before making any payment.

How to Stop the Debt Collector Harassment

You know you can tell them to stop calling. But simply saying 'Stop' over the phone rarely works. You need to create a paper trail that holds up in court.

The Cease and Desist Letter

As per Federal law, if you send a Cease and Desist letter to the third - party debt collector to stop all communication with you, they must stop (unless they are mailing you legal papers).

The 'Green Postcard' Strategy

- Go to the Post Office.

- Send the letter via Certified Mail with Return Receipt Requested.

- You will get a green postcard back with their signature on it.

That green card is your proof. If they call you again after signing that card, they have violated the FDCPA. You can now sue them for $1,000 per violation plus your attorney fees.

What To Do If The Debt Collector Sues You

If you receive a summons and petition from the court, you have been sued. Do not panic, do not hide, or ignore the summons.

If you ignore the lawsuit, the judge will issue a 'Default Judgment.' This means the collector wins automatically. They can now freeze your bank account and garnish your wages without asking permission again.

What to do:

- Read the Petition - Who is suing you? Is it the original bank or a debt buyer?

- File a Response - You usually have 21 days to file a formal answer with the Clerk of the Court. You don't need a fancy lawyer letter. You can often find a simple 'Answer' form at your state's courthouse.

-

Check the Box - On the form, you typically just need to deny the debt. This forces the debt collector to show up in court and prove:

- They own the debt.

- The amount is correct.

- The statute of limitations hasn't expired.

Court Costs and Timeline to Expect

Filing an Answer typically costs between $40 and $200 in Kansas, depending on the court and the amount of the claim. The process from filing to resolution usually takes 3 to 6 months, though contested cases can take longer.

Should You Hire an Attorney?

If the debt amount is large (over $5,000) or the case is complex, consulting with an attorney may be worthwhile. Many consumer law attorneys offer free initial consultations and work on contingency if the collector has violated the law. For smaller debts, you can often handle the process yourself using court - provided forms.

Debt Payments - Whom Do You Pay First

If you have to pay debts in collections, you need a plan for that. When looking at debt collection laws in Kansas, here is the order you may follow to manage payments:

Priority 1:

- Car Loan - In Kansas, they can repossess your car quickly if you miss the 'Right to Cure' window. If you need your car for work, pay this before your credit cards.

- Child Support/Taxes - The government has special powers to take your money. So, pay them asap.

Priority 2:

- Credit Cards & Medical Bills - These unsecured debts will be your next target. They cannot take your house or car without suing you first. It will take time, so keep negotiating for the payment.

How Debt Settlement Works in Kansas

If you have some money left in your hand, but can't pay your outstanding debts in full, you might want to settle them. This means you can offer debt collectors a lump sum - often 40% to 60% of the original balance - to pay off the debt once and for all.

If you choose a debt settlement company in Kansas, it must be registered with the Office of the State Bank Commissioner (OSBC). Check their license before you sign anything.

Impact on Your Credit Report

Debts in collection can remain on your credit report for up to 7 years from the date of the first missed payment, even after the Kansas statute of limitations on debt collection has expired. Here is what you should know:

- Paid collections: Paying off a collection account does not automatically remove it from your report, but it updates the status to 'paid,' which some lenders view more favorably.

- Settled debts: If you settle for less than the full amount, your report will show 'settled' rather than 'paid in full.' This can still affect your credit score, but it resolves the balance.

- Medical debt changes: As of 2023, paid medical collections are removed from credit reports, and medical debts under $500 are no longer reported.

- Disputing errors: If a collector reports inaccurate information, you can dispute it directly with the credit bureaus (Equifax, Experian, TransUnion). They must investigate within 30 days.

Frequently Asked Questions (FAQ)

In Kansas, collectors generally have 5 years to sue for written contracts and 3 years for accounts like credit cards. After that time passes, they can ask you to pay, but they cannot legally take you to court to force you to pay.

You do not have to pay unless the collector proves the debt is valid, accurate, and within the legal time limit. You also have the right to verify the debt is real or negotiate a settlement before paying anything.

You cannot go to jail simply for not paying consumer debts like credit cards, personal loans, or medical bills. Being in debt is a civil issue, not a crime that leads to arrest.

Kansas law usually limits extra collection fees and attorney costs to 15% of the total debt you owe. If a collector tries to charge huge extra service fees, they are likely breaking the law.

They must prove they have the legal right to collect the money, show exactly how much you owe (including any fees), and provide the original contract or history to prove the debt is real.

Kansas limits wage garnishment to 25% of your disposable income OR the amount above $217.50 per week (30 times the federal minimum wage), whichever is less. If you earn $217.50 or less per week, your wages cannot be garnished at all.

Before repossessing your car or demanding full loan payment, Kansas creditors must send a 'Right to Cure' notice under K.S.A. 16a - 5 - 110. This gives you 20 days to catch up on missed payments. If you pay the past - due amount within this period, your account is restored to good standing.

Yes. You can send a cease and desist letter to third - party debt collectors demanding they stop contacting you. Send it via certified mail with return receipt requested. Once received, they must stop calling except to notify you of legal action. If they continue calling, they have violated the FDCPA, and you can sue for damages.

The Bottom Line

Dealing with debt collectors is incredibly stressful, but Kansas law equips you with powerful protections like the Uniform Consumer Credit Code to actively fight back against harassment and unfair practices. These regulations protect a portion ($217.50) of your paycheck from garnishment, mandate a 20 - day 'Right to Cure' notice before property repossession, and enforce strict Kansas statute of limitations on debt collection that can legally kill old 'zombie' debts.

Never ignore a court summons, absolutely avoid making small payments that accidentally revive expired debts, and use certified cease - and - desist letters to legally force collectors to stop calling.

Ready to See Your Options?

Attorney Lyle Solomon and the team at Oak View Law Group have helped more than 7,600 people successfully resolve their outstanding debt problems. The consultation is completely free, and there is absolutely no obligation to move forward until you are ready.

👉 Request a Free Consultation | - Take the Debt Relief Suitability Assessment Call (800) 530 - OVLG

Helpful Resources:

- Report a Lender (OSBC): Office of the State Bank Commissioner of Kansas

- Kansas Statute on Written Contracts (K.S.A. 60 - 511) - The official state law establishing a 5 - year time limit for filing lawsuits on written agreements and promissory notes.

- Kansas Statute on Unwritten Contracts (K.S.A. 60 - 512) - The official state law establishing a 3 - year time limit for lawsuits regarding oral contracts and open - ended accounts.

- Kansas Judgment Dormancy Law (K.S.A. 60 - 2403) - Explains how long a court judgment remains valid in Kansas and when it becomes 'dormant' or uncollectible.

- Notice of Consumer's Right to Cure (K.S.A. 16a - 5 - 110) - Kansas law requires lenders to give borrowers a specific notice and time to pay past - due amounts before taking further action.

- Kansas Consumer Protection Act - Deceptive Practices (K.S.A. 50 - 623) - Statutes protecting consumers from unfair, unconscionable, or deceptive business and collection practices.

- Uniform Consumer Credit Code (UCCC) Resources - K.S.A. Chapter 16a - Information and legal forms regarding the specific code that governs consumer credit transactions and limitations.

- Understanding 'Zombie Debt' - A guide explaining old debts that collectors try to revive after the legal time limit has expired.

- Kansas Wage Garnishment Restrictions (K.S.A. 60 - 2310) - State laws that limit how much of a worker's paycheck can be seized by creditors to pay off debts.

- Federal Wage Garnishment Laws (Fact Sheet #30) - U.S. Department of Labor guidelines on the Consumer Credit Protection Act (CCPA) limits for wage garnishment.

- Kansas Attorney General Consumer Protection - File a complaint or learn about your rights.

- Kansas Hospital Association - No Surprises Act - Information on federal protections that prevent patients from receiving unexpected bills from out - of - network providers.

- Kansas Charitable Health Care Provider Program - A directory and information for clinics that provide free or low - cost medical care to eligible low - income residents.

- KanCare (Medicaid) Program Updates - News and eligibility information regarding Kansas's state Medicaid program for low - income individuals.

- Sample Hospital Charity Care Policy - An example of a financial assistance policy showing how hospitals determine eligibility for free or discounted care.

- Fair Debt Collection Practices Act (FDCPA) - Full text and resources from the Federal Trade Commission.

Disclaimer

This information is provided for educational purposes only and does not constitute legal advice. Debt collection laws are complex and can change. For specific legal questions about your situation, consult with a qualified attorney. Oak View Law Group (OVLG) is a law firm that provides debt relief services and consumer assistance. Free consultations are available; service fees apply to enrolled programs. See OVLG's refund policy for details