Lyle Solomon

Lyle Solomon

Loretta Kilday

Loretta Kilday

Updated: • 16 min read

Stop Collector Abuse Through Indiana Debt Collection Laws

- Statute of limitations: 6 years for unwritten (oral) contracts, 6-10 years for written contracts depending on type.

- Wage garnishment: 25% of disposable income; judgment can be renewed for another 10 years, extending collection period.

- Collectors cannot mislead you about government affiliation, threaten legal action they won't take, or use foul language.

- You can request debt validation in writing and dispute errors before making payment.

- Collectors cannot use harassment, false threats, or deceptive claims while collecting debt.

Key Takeaways

- Third-party debt collectors are strictly forbidden from using abusive, deceptive, or unfair practices under the Fair Debt Collection Practices Act (15 U.S.C. § 1692) and Indiana debt collection laws.

- The statute of limitations on most Indiana debts is six years for credit cards, medical bills, and written contracts, under Indiana Code Title 34, Article 11, Chapter 2. Making even one small payment can restart this clock.

- Indiana wage garnishment laws protect at least 75% of your disposable earnings. Senate Bill 197 (pending) would raise that floor even higher, and Senate Bill 225, signed March 2026, shields you from hospitals that violate pricing transparency rules.

- If a collection agency breaks these rules, you have the right to sue for actual damages plus up to $1,000 in statutory penalties per lawsuit, along with attorney fees.

- Indiana bankruptcy exemptions let you keep up to $22,750 of equity in your home and a $12,100 wildcard exemption for your vehicle.

Indiana consumers filed more than 6,000 debt collection complaints with the CFPB between January 2025 and March 2026, making it one of the most common financial complaints filed in the state (Source: CFPB Consumer Complaint Database, 2025–2026). Roughly 23% of Indiana adults carry at least one debt in collections, just above the national average of 22% (Source: Urban Institute, Debt in America, August 2025).

Knowing your rights under Indiana law can help you stop illegal collection tactics. This guide walks you through what collectors can and cannot do, how long they have to sue you, and the exact steps you can take today to make the phone calls stop.

Quick Reference: Indiana collectors must be licensed by the Indiana Secretary of State. They cannot call before 8 AM or after 9 PM, threaten you with jail, or lie about what you owe. Violations can cost them up to $1,000 in statutory damages per lawsuit, plus your actual damages and attorney fees.

The FDCPA and State Protections

When a debt collector contacts you, they must follow a strict legal code of conduct. At the federal level, the Fair Debt Collection Practices Act (FDCPA) was created by Congress specifically to stop collectors from using threatening or deceptive tactics against consumers.

Indiana adds its own layer of protection through the FDCPA along with the Indiana Uniform Consumer Credit Code (IUCCC), Indiana Code § 24-4.5. Under the Indiana Collection Agency Act, every third-party collection agency must hold a valid license issued by the Indiana Secretary of State before they can legally collect a debt in this state. If they do not have that license, every communication they have sent you is arguably unlawful and that gives you real leverage.

Check the Secretary of State's database before your next conversation with a collector. If they are unlicensed, document it immediately.

What Debt Collectors Are Forbidden to Do

The rules under Indiana law and the FDCPA ban harassment and abuse outright. A collector cannot:

- Threaten you physically or threaten to damage your property or reputation

- Shame you publicly—putting your name on a “deadbeat” list or telling your neighbors, friends, or family members about your debt

- Use foul or abusive language, including profanity or discriminatory slurs, in calls or letters

- Call repeatedly with the intent to annoy or pressure you

- Call outside legal hours—before 8:00 AM or after 9:00 PM in your local time zone.

- Call your workplace after you tell them your employer does not allow personal calls

- Lie about who they are, pretend to be police, claim you committed a crime, or threaten you with arrest—debt is a civil matter, and there are no debtor's prisons in the United States.

Real example: A collector tells you, "If you don't pay by Friday, we're sending the sheriff to your house." That is illegal. Document the exact date, time, and wording. It is a textbook FDCPA violation.

Indiana vs. Federal Protections - Which Is Stronger?

Both laws work together, but they cover different ground:

| Federal vs. Indiana Protections at a Glance | ||

|---|---|---|

| Protection Area | Federal FDCPA | Indiana State Law |

| Who it covers | Third-party collectors only | All licensed collection agencies |

| Original creditors covered? | No | Partially — under IUCCC |

| Licensing required | No | Yes — Secretary of State |

| Calling hours restriction | 8 AM – 9 PM | 8 AM – 9 PM |

| Statutory damages | Up to $1,000 per lawsuit | Additional penalties under IUCCC |

| Where to file complaints | CFPB / FTC | Indiana Attorney General |

| Medical debt protections | No special rules | SB 225 blocks collection for pricing transparency violations |

| Can you use both? | Yes – file under both laws simultaneously | Yes – file under both laws simultaneously |

Check the Secretary of State's database to verify a collector's license. If they are unlicensed, every communication they have sent is arguably unlawful, giving you additional leverage.

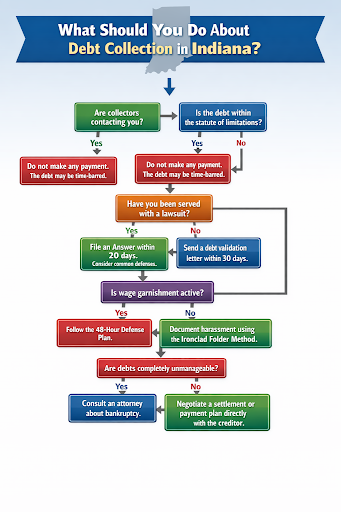

Statute of Limitations on Debt in Indiana

Indiana law limits how long creditors can sue you for old debts. Once the time limit expires, the debt becomes "time-barred," meaning a court will not enforce a collection lawsuit against you.

Statute of Limitations by Debt Type

| Debt Statute of Limitations in Indiana | ||

|---|---|---|

| Debt Type | Time Limit | Common Examples |

| Open-ended accounts | 6 years | Credit cards, medical bills |

| Oral / unwritten contracts | 6 years | Verbal loan agreements |

| Written contracts (payment of money) |

6 years | Personal loans, promissory notes |

| Written contracts (other purposes) |

10 years | Service agreements, business contracts |

| Sale of goods | 4 years | Auto loan deficiencies after repossession |

| Court judgments | 10 years (renewable) | Can be renewed for another 10 years |

| Source: Indiana Code Title 34, Article 11, Chapter 2 | ||

The Restart Trap

Be careful when speaking to collectors about old accounts. Paying even a small amount can restart the statute of limitations, giving the creditor a fresh window to sue you. Even sending a letter that acknowledges the debt is yours can reset the clock to day one.

For example, you owe $3,000 on a credit card from 2018. The six-year window is almost up. A collector calls and asks you to “just pay $25 as a goodwill gesture.” If you do, Indiana law may treat that as a new payment, restarting the full six-year period. That $25 just gave them until 2031 to sue you.

Avoiding Accidental Debt Revival in Indiana

A critical part of consumer protection is the legal timeframe in which a creditor can take you to court. If a debt is too old, it becomes 'time-barred.' This means the court will no longer let the collector win a judgment against you.

Indiana law limits how long creditors can sue you for old debts. This timeline is found in Indiana Code Title 34, Article 11, Chapter 2 and varies based on the type of agreement you made with the original lender.

Indiana Wage Garnishment Laws

If a creditor wins a judgment against you, they can ask the court to garnish your wages directly from your paycheck. Indiana law protects most of your income.

What do disposable earnings mean?

Your gross pay minus legally required deductions for federal and state taxes, Social Security, and Medicare. Voluntary deductions like 401(k) contributions or health insurance premiums are not subtracted. This means your disposable earnings figure is often higher than your actual take-home pay.

Attorney Nick Heimlich, owner of Nick Heimlich Law, warns that “disposable income is defined as what is left after taxes and other legally required amounts have been deducted, and miscalculating disposable income is fairly common.” Before your hearing, demand the creditor's exact worksheet and check their math.

How Much Can Creditors Take?

A creditor can only garnish whichever amount is less:

- The 25% Rule: Up to 25% of your disposable weekly earnings.

- The Minimum Wage Rule: The amount by which your disposable weekly earnings exceed 30 times the federal minimum wage ($217.50).

- The Hardship Exception: If you prove extreme financial hardship, a judge can reduce garnishment to as low as 10%.

- SB 197 (Pending): Would raise protection from 30× to 83× minimum wage, shielding the first $601.75 of your weekly check.

- SB 225 (Active): Signed March 2026, Senate Bill 225 forbids hospitals and third-party agencies from pursuing medical debt if the hospital violated state pricing transparency laws.

According to Ali Zane, CEO of IMAX Credit Repair & Identity Theft Lawyer, acting fast is your best weapon. 'In Indiana, creditors may garnish only 25% of the debtor's earnings or the amount exceeding 30 times the minimum wage, whichever is lower,' Zane explains. 'In the end, the debtor can keep a large chunk of the money they earn. The debtor must take action quickly by asserting the hardship defense.'

The 48-Hour Garnishment Defense Plan

To stop wage garnishment in Indiana, act before the court order hits your employer's payroll. Follow this plan within 48 hours of receiving your notice:

Find Your Case Number

Check the top right corner of your garnishment notice. Write down the court case number and county judge name. You need this for every document you file.

File a Hardship Objection

Go to the county clerk's office and file a “Claim for Exemption and Request for Hearing.” Attach rent receipts, grocery bills, and utility statements proving the 25% deduction will leave you unable to cover basic living expenses.

Audit the Creditor's Math

Demand the exact worksheet the creditor's attorney used to calculate your disposable earnings. Math errors on mandatory payroll deductions are common and grounds to dismiss the order.

Offer a Direct Payment

Call the creditor's lawyer directly for debt settlement. Say, I am filing a hardship exemption today, but I will agree to a voluntary direct payment of $50/month if you drop the garnishment order.

Trigger the Automatic Stay

If they refuse, consult an attorney about filing a Chapter 7 or Chapter 13 bankruptcy petition. The automatic stay forces your employer to stop deductions immediately.

How to Respond to a Debt Collection Lawsuit in Indiana

If a collector files a lawsuit against you, do not ignore it. Failing to respond results in a default judgment, meaning the creditor automatically wins and can immediately garnish your wages or levy your bank account.

Your Response Timeline

- You have 20 calendar days after being served to file a written answer with the court (Indiana Trial Rule 6).

- Small claims cases (debts under $10,000) follow simplified procedures; you appear and argue your case directly before a judge.

Common Defenses You Can Raise

- Expired statute of limitations: The creditor waited too long to sue.

- Wrong person: The debt does not belong to you.

- Incorrect amount: The balance includes unauthorized fees or interest.

- Lack of standing: A debt buyer cannot prove they legally own your debt.

- No valid license: The collector is not licensed by the Indiana Secretary of State.

If you cannot afford an attorney, contact Indiana Legal Services for free assistance or visit your county's self-service legal center for answer form templates.

Indiana Bankruptcy Exemptions

When debts become unmanageable, filing for bankruptcy can provide a fresh start. Indiana requires residents to use state-specific exemption amounts, not the federal list.

Key Exemption Amounts (2026)

- Homestead: $22,750: Protects equity in your primary home. Married couples can double this to $45,500.

- Wildcard: $12,100: Indiana has no specific vehicle exemption, so apply this to protect car equity or valuable household goods.

- Bank Accounts: $450: Protects cash and bank deposits. SB 197 would raise this to $1,500.

- Retirement: 100% Protected: 401(k)s, IRAs, and pensions are fully shielded.

- Health Aids & Benefits: Prescribed health aids, unemployment compensation, and certain life insurance policies are exempt.

Do not transfer assets or move money to hide it before filing. Courts treat this as fraud and it can destroy your case. Consult a qualified attorney before submitting any bankruptcy petition.

How to Validate Debt in Indiana

Before paying anything, verify the debt is yours and the amount is correct.

- Within 5 days of first contact, a collector must send written notice showing the amount owed, the original creditor's name and your right to dispute.

- You have 30 days to send a written dispute letter.

- Once you dispute, the collector must stop all collection activity until they provide verification, original account statements, proof the debt is yours and proof they are licensed in Indiana.

As Nick Heimlich explains, this process does more than just pause the calls. 'Collectors must validate the debt prior to continuing collection action, which gives consumers leverage for negotiating.'

What to include in your validation letter:

- Your name and address

- The account number from their notice

- A clear statement: 'I dispute this debt and request full validation under 15 U.S.C. § 1692g.'

- Send it via certified mail with return receipt so you have proof of delivery.

If the collector cannot validate the debt, they cannot legally continue collecting.

Debt Collection and Your Credit Report

Collection accounts can devastate your credit score, but Indiana consumers have specific rights:

- 7-Year Rule: Collection accounts appear on your credit report for up to seven years from the date of your first missed payment regardless of whether the statute of limitations is shorter.

- Medical Debt Protections: Paid medical collections are removed from credit reports. Unpaid medical debts under $500 no longer appear (effective 2023 credit bureau policy changes).

- Dispute Inaccurate Accounts: If a collection account contains errors—wrong balance, wrong name, debt you already paid—file disputes with all three credit bureaus (Equifax, Experian, TransUnion) under the Fair Credit Reporting Act.

- Paid vs. Settled: A “paid in full” notation helps your score more than “settled for less than owed.” Negotiate the reporting language before you pay.

Important: The 7-year credit reporting clock and the statute of limitations are separate timelines. A debt can fall off your credit report but still be legally collectible or vice versa.

What to Do When Collectors Contact Your Employer or Family

One of the most stressful tactics collectors use is calling people you know. Here is exactly what Indiana and federal law allow:

Regarding your employer:

- A collector may call your workplace only to locate you (called a 'location call'), and even then, they cannot reveal that you owe a debt.

- If you tell them, verbally or in writing, that your employer prohibits personal calls, they must stop calling your workplace immediately.

- If they continue calling after you notify them, each call is a separate FDCPA violation.

Regarding family and friends:

- Collectors can contact third parties once to find your phone number or address.

- They cannot tell anyone, parents, siblings, neighbors, that you owe money.

- They cannot call the same person more than once unless that person asks them to call back.

If a collector violates any of these rules, log it in your documentation folder and file complaints with both the CFPB and the Indiana Attorney General.

The Ironclad Folder Method to Stop Harassment

To stop collection harassment under Indiana law, you need documented proof. This five-step framework builds your case and gives you the right to sue.

The Dedicated Notebook

Keep a notebook by your phone. Every time a collector calls, write down the date, exact time, agent's name, phone number used, and exactly what they said or threatened. Save every voicemail, text, and letter.

The Cease-and-Desist Letter

Mail a certified letter stating: “Under the FDCPA, I am formally requesting that you cease all communication with me regarding this account. Do not call my home, my cell phone, or my workplace.”

As Ali Zane, CEO of IMAX Credit Repair & Identity Theft Lawyer, confirms, “They are not allowed to contact you if you have sent a written request to cease communication.”

📋 [Download Our Free Cease-and-Desist Letter Template]

The 30-Day Validation Demand

Within 30 days of their first contact, send a letter demanding they prove you owe the money. By law, they must stop all collection activity until they mail back original statements and proof of their Indiana license.

Report to the CFPB

Take photos of your notebook pages and upload them to the CFPB complaint portal. Federal regulators actively use these logs to fine abusive agencies.

File with the Indiana Attorney General

Send copies of your folder to the Indiana Attorney General's Consumer Protection Division. They have the authority to revoke the agency's state operating license.

Frequently Asked Questions

Collectors typically have six years to sue for credit card debt, medical bills, and most written contracts. After the statute of limitations expires, the debt is time-barred and courts will not enforce collection lawsuits. However, if a judgment already exists, it remains valid for ten years and can be renewed.

Indiana law protects at least 75% of your disposable weekly earnings. Creditors can only take 25% of your disposable income or the amount above $217.50 per week (30 times the federal minimum wage), whichever is less. If Senate Bill 197 passes, the protected floor rises to $601.75 per week.

Yes, unless you tell them your employer prohibits personal calls. Once you notify them in writing, they must stop. Each additional workplace call after that written notice is a separate FDCPA violation.

Document the threat immediately and file complaints with both the Indiana Secretary of State and the Consumer Financial Protection Bureau. Under the Fair Debt Collection Practices Act, you can also sue for up to $1,000 in damages plus attorney fees.

Yes. Under Senate Bill 225, signed March 2026, if a hospital failed to comply with state pricing transparency laws, neither the hospital nor a third-party agency can legally pursue you for that specific medical debt.

Independent contractors (1099 workers) do not receive a traditional W-2 paycheck, so standard wage garnishment orders do not apply. Instead, creditors typically seek a non-wage garnishment to take money directly from your bank account. If you are a 1099 worker facing collection action, speak with an attorney about protecting your bank deposits.

Bottom Line

If you are facing debt collection in Indiana, you have strong legal protections under both federal and state law. Violations can cost collectors $1,000 per incident. Time limits protect you from old debts. Significant portions of your income and assets remain shielded even in worst-case scenarios.

Act quickly, file hardship objections, validate disputed debts, document harassment and explore all resolution options. Oak View Law Group helps Indiana residents understand their rights and develop strategies that work for their specific situation.

Helpful Resources

To verify licenses, read statutes, and file formal complaints, use these official sources:

- Can debt collectors collect a debt that's several years old, Know your options.

- The Indiana Uniform Consumer Credit Code (IUCCC), Indiana Code § 24-4.5, State laws regulating consumer loans, credit sales, and leases.

- Read the Official Indiana Code: Title 34, Article 11, Exact legal text for statute of limitations.

- File a State Complaint, Submit a formal grievance to the Indiana Attorney General's Consumer Protection Division.

- File a Federal Complaint, Upload harassment logs and report abusive tactics to the CFPB.

- Learn About the FDCPA, Plain-English breakdown of your federal rights from the FTC.

- Fair Debt Collection Practices Act, 15 U.S.C. § 1692, Federal Trade Commission

- Indiana Secretary of State, Collection Agency Licensing, State of Indiana

Disclaimer

This information is provided for educational purposes only and does not constitute legal advice. Debt collection laws are complex and can change. For specific legal questions about your situation, consult with a qualified attorney. Oak View Law Group (OVLG) is a law firm that provides debt relief services and consumer assistance. Free consultations are available; service fees apply to enrolled programs. See OVLG's refund policy for details