Key Takeaways

- Filing for bankruptcy triggers an automatic stay that stops repossession the moment your petition reaches the court.

- A Chapter 13 cramdown can cut your loan balance to what the car is actually worth, erasing negative equity.

- You must have purchased the vehicle at least 910 days before filing to qualify for a cramdown.

- Chapter 7 redemption lets you pay the car's current market value in one lump sum and walk away from the rest.

- Reaffirmation keeps your original loan terms intact, which means you keep the debt and the risk.

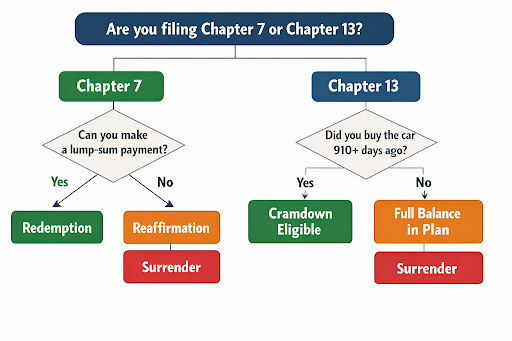

If your auto loan balance is thousands more than your car is worth, bankruptcy gives you a few concrete ways to fix that. Which option works depends on whether you file Chapter 7 or Chapter 13.

Both chapters trigger an automatic stay under 11 U.S.C. § 362 the moment your petition is filed. That federal order prohibits your lender from repossessing, calling, or suing you while the case is open. In a Chapter 7 case, the stay typically lasts 3 to 6 months. In Chapter 13, it lasts the full 3 to 5 years of your repayment plan, unless the lender successfully asks the court to lift it. Violation of automatic stay has severe consequences.

“The moment your case is filed, the automatic stay acts as an immediate legal wall that forces the repo agent to back down. It buys you the critical time needed to breathe, but remember you still must execute a court-approved plan to catch up on arrears if you want to keep the car long-term”.

| Option | Chapter | Who Qualifies | What Happens | Main Risk |

|---|---|---|---|---|

| Cramdown | 13 | Bought car 910+ days before filing | Loan balance reduced to car's current market value; interest rate lowered | 3 to 5 year plan commitment; missed payments can trigger dismissal |

| Redemption | 7 | Any individual debtor with a secured car loan | Pay lender the car's current value in one lump sum; remaining balance wiped | Requires full payment at once; redemption lenders charge high interest |

| Reaffirmation | 7 | Any debtor willing to keep original loan terms | Sign new agreement keeping the same loan; keep making payments | Full personal liability stays; lender can repossess and sue if you default later |

| Surrender | 7 or 13 | Anyone | Return the car; remaining debt discharged | You lose the vehicle |

How a Chapter 13 Cramdown Reduces What You Owe

The cramdown is the single most effective tool for lowering a car payment through bankruptcy. The court resets your secured loan balance to match the car's current market value. The leftover amount gets lumped in with your unsecured debts, and you pay only a fraction of it through your repayment plan.

Say you owe $18,000 on a car that is worth $12,000 today. A cramdown would reduce your secured balance to $12,000. The remaining $6,000 becomes unsecured debt, treated the same as credit card balances.

The interest rate drops too. Under the formula from Till v. SCS Credit Corp., 541 U.S. 465 (2004), bankruptcy courts start with a national prime rate and add a risk adjustment, typically 1% to 3% depending on the court's assessment. The Federal Reserve H.15 release shows the prime rate at 6.75% as of April 2026. A cramdown rate might land somewhere between 7.75% and 9.75%, compared to the 18% or 22% rate on a typical subprime auto loan.

The repayment gets stretched across the full length of your Chapter 13 plan, which runs either 36 or 60 months depending on your income.

How to Check if You Qualify for a Cramdown

There is one hard eligibility rule under 11 U.S.C. § 1325(a)(9), you must have purchased the vehicle at least 910 days (about two and a half years) before your filing date. Congress added this requirement to prevent people from buying a new car and immediately filing to get the balance slashed.

To check your eligibility, pull out your purchase contract and count the days. Then look up your car's current trade-in value on Kelley Blue Book. Call your lender or log into their site to get your exact payoff balance. If the payoff is higher than the value and you pass the 910-day test, you are in cramdown territory.

If you bought the car less than 910 days ago, the cramdown is off the table. You would still file your Chapter 13 plan with the full loan balance as a secured claim, but you would not get the balance reduction.

What Chapter 7 Does for Your Car Loan

Chapter 7 bankruptcy is one of the debt relief options, that wipes out your personal obligation to pay the loan. Your lender cannot sue you for the balance. But the lien on the car survives, so the lender can still take the vehicle unless you take one of two steps: redemption or reaffirmation.

Redemption

Under 11 U.S.C. § 722, you can buy your car outright by paying the lender its current market value in a single lump-sum payment. If you owe $15,000 but the car is worth $7,000, you pay $7,000 and the rest is gone.

Most people do not have $7,000 sitting around during a bankruptcy, which is where redemption lenders come in. Companies like 722 Redemption Funding specialize in lending to people in active Chapter 7 cases. The catch is the interest rate. These loans often carry rates in the high teens or low twenties because the borrower is mid-bankruptcy.

Before signing with a redemption lender, ask your attorney to compare the total cost of the redemption loan (principal plus interest over the full term) against what you would pay by reaffirming the original loan. In some cases, the redemption loan costs more over time even though the principal is smaller.

A bankruptcy judge must approve the redemption to confirm the valuation is accurate and the lender is getting fair market value.

Why Reaffirmation Rarely Lowers Your Payment

Reaffirmation means you sign a new agreement with your lender agreeing to keep the original loan alive. The bankruptcy discharge will not apply to that debt. You keep making payments on the same terms.

Lenders almost never agree to lower the rate or balance as part of a reaffirmation. They do not have to. You are the one asking to keep the car, and they already have the lien. So in most cases, reaffirmation does not lower your payment at all.

The real danger is what happens after the case closes. If you lose your job, get hit with a medical bill, or fall behind, the lender can repossess the car and sue you for the deficiency. You gave up your discharge protection on that debt when you signed the agreement.

“Signing a reaffirmation agreement essentially waives your bankruptcy protection for that specific debt, putting you fully back on the hook. If your finances take a hit later and you default, the creditor can repossess the asset and sue you for the remaining deficiency balance.”

Many bankruptcy judges will refuse to approve a reaffirmation if the debtor's budget shows the payments are not affordable. The court views this as a safety check.

Cramdown Math

When Giving the Car Back Makes the Most Sense

If the car needs expensive repairs, or the loan balance is far more than the vehicle is worth, surrender may be the cleanest option. You return the car. The bankruptcy discharge wipes out whatever you still owe. You walk away with no deficiency balance.

This is worth considering if your repair costs would exceed two months of payments, or if your negative equity is above $5,000. The money you save by not making car payments can go toward buying a cheaper vehicle with cash after your case closes.

What Bankruptcy Costs and How Long It Takes

Before choosing a chapter, factor in the cost of the filing itself.

Chapter 7: The court filing fee is $338. Attorney fees typically run $1,000 to $2,500 depending on location and complexity. The case usually closes in 3 to 6 months.

Chapter 13: The court filing fee is $313. Attorney fees run higher, generally $3,000 to $5,000, because the attorney has to prepare a multi-year repayment plan and manage the case for its full duration. The plan runs for 36 or 60 months.

Means test: Not everyone qualifies for Chapter 7. Federal law requires a means test that compares your household income to the median for your state. If your income is too high, you may be required to file Chapter 13 instead.

Credit report impact: A Chapter 7 filing stays on your credit report for 10 years from the filing date. Chapter 13 stays for 7 years. Many people begin rebuilding within 12 to 24 months of discharge by using secured credit cards and making on-time payments.

Missed Chapter 13 payments: If you fall behind on your plan payments, the trustee can move to dismiss your case. Once dismissed, the automatic stay lifts and your lender can resume repossession. Contact your attorney immediately if you cannot make a payment.

How State Exemption Laws Protect Your Car

Before a cramdown or redemption can help, you need to make sure the court will not sell your car to pay unsecured creditors. That depends on your state's vehicle exemption, which sets a dollar limit on how much equity you can protect.

If you own the car outright and it is worth more than your state's exemption, the Chapter 7 trustee could sell it, pay you the exempt amount, and distribute the rest to creditors. If your equity is below the limit, the car is protected.

The table below shows vehicle exemption amounts for several states. These figures are current as of April 2026, but exemptions change periodically. Confirm the current amount with a licensed attorney in your state before filing.

| State | Vehicle Exemption | Key Statute |

|---|---|---|

| California (System 1) | $8,625 | Cal. Civ. Proc. § 704.010 |

| California (System 2) | $8,625 | Cal. Civ. Proc. § 703.140(b)(2) |

| Texas | Unlimited (one per licensed member) | Tex. Prop. Code § 42.002 |

| Florida | $5,000 | Fla. Stat. § 222.25(1) |

| New York | $4,000 | N.Y. DCL § 282(1) |

| Illinois | $3,600 (eff. Jan 1, 2026) | 735 ILCS 5/12-1001(c) |

| Utah | $5,000 | Utah Code Ann. § 78B-5-506 |

Many states also offer a wildcard exemption you can stack on top of the vehicle exemption if your car's equity exceeds the standard limit. A bankruptcy attorney in your state can calculate exactly how much protection is available.

Frequently Asked Questions

Yes. The automatic stay takes effect the moment your petition is filed. Your lender must stop all collection activity, including repossession, until the stay is lifted or the case closes.

A Chapter 13 cramdown. The court resets your secured balance to the car's current market value and wipes out the negative equity. It also reduces your interest rate using the Till formula.

No. Under 11 U.S.C. § 1325(a)(9), the vehicle must have been purchased at least 910 days before your filing date. If you bought it more recently, the full loan balance remains a secured claim in your plan.

Yes, through either redemption or reaffirmation. Redemption lets you pay the car's current value in a lump sum and eliminate the remaining balance. Reaffirmation keeps your original loan terms in place.

In most cases, no. Reaffirmation puts you back on the hook for the full debt. If you default after the case closes, the lender can repossess the car and sue you for whatever you still owe. The discharge you received in bankruptcy will not protect you on that particular debt.

In Chapter 7, the stay usually lasts 3 to 6 months until the case closes. In Chapter 13, it lasts the full 3 to 5 years of the repayment plan. Your lender can ask the court to lift the stay early if you are not making payments or if the car is losing value.

The trustee can file a motion to dismiss your case. If the court grants it, the automatic stay lifts and your lender can immediately resume repossession. Call your attorney as soon as you know you will miss a payment. Some courts allow plan modifications to address temporary financial setbacks.

Chapter 7 remains on your credit report for 10 years. Chapter 13 remains for 7 years. The initial drop varies by person, but many filers see their scores start to recover within 12 to 24 months as they use secured credit cards and maintain on-time payments.

The Bottom Line

If your car loan balance is far above what the vehicle is worth, you are not stuck with it. A Chapter 13 cramdown can cut the balance to market value, lower the interest rate, and spread payments over 3 to 5 years. Chapter 7 redemption lets you buy the car for what it is actually worth today, though you will need a lump sum or a redemption lender to do it.

Reaffirmation rarely helps. Surrender makes sense when the math does not justify keeping the car.

The right move depends on your income, your car's value, how long you have owned it, and your state's exemption laws. Gather your loan documents, check your vehicle's trade-in value on Kelley Blue Book, and take those numbers to a bankruptcy attorney in your area. Most offer free initial consultations.

Looking for Help With Your Debt?

Attorney Lyle Solomon and the team at Oak View Law Group have helped thousands of people resolve their debt. The consultation is free, and there is no obligation to move forward.

Request a Free Consultation | Call (800) 530-OVLG

Helpful Sources:

- 11 U.S.C. § 362 - Automatic Stay

- 11 U.S.C. § 722 - Chapter 7 Redemption

- 11 U.S.C. § 1325(a)(9) - 910-Day Rule

- Till v. SCS Credit Corp., 541 U.S. 465 (2004) - Supreme Court ruling on Chapter 13 interest rates

- Federal Reserve H.15 Statistical Release - Prime rate data

- U.S. Courts Bankruptcy Fee Schedule

- Cal. Civ. Proc. § 704.010 - California motor vehicle exemption (System 1)

- Cal. Civ. Proc. § 703.140(b)(2) - California motor vehicle exemption (System 2)

- Tex. Prop. Code § 42.002 - Texas personal property exemptions

- Fla. Stat. § 222.25(1) - Florida motor vehicle exemption

- N.Y. Debtor & Creditor Law § 282(1) - New York bankruptcy motor vehicle exemption

- 735 ILCS 5/12-1001(c) - Illinois motor vehicle exemption (amended by P.A. 104-0120, eff. Jan 1, 2026)

- Utah Code Ann. § 78B-5-506 - Utah motor vehicle exemption

- Kelley Blue Book - Vehicle valuation reference

Disclaimer: This article provides general information about how bankruptcy may affect your auto loan and should not be construed as legal advice. If you are considering bankruptcy to address an auto loan or other debt, consult with a qualified bankruptcy attorney who can evaluate your specific circumstances. Oak View Law Group provides debt relief services and offers free consultations to help you understand your options. Service fees apply to enrolled programs. Individual results vary based on debt amount, creditor cooperation, and financial circumstances. See OVLG's refund policy for details.