Lyle Solomon

Lyle Solomon

Loretta Kilday

Loretta Kilday

Updated: • 17 min read

Debt Collection Laws in Nebraska and Your Legal Remedies

- Under debt collection laws in Nebraska, abusive behavior from a debt collector, such as threats, late-night calls, or lies about jail time, is illegal.

- If you support a family, you might be able to protect 85% of your paycheck from garnishment, rather than the standard 75%. Most people miss this.

- The Nebraska statute of limitations on written contracts is 5 years. If the debt is older than that, they cannot legally force you to pay through the courts.

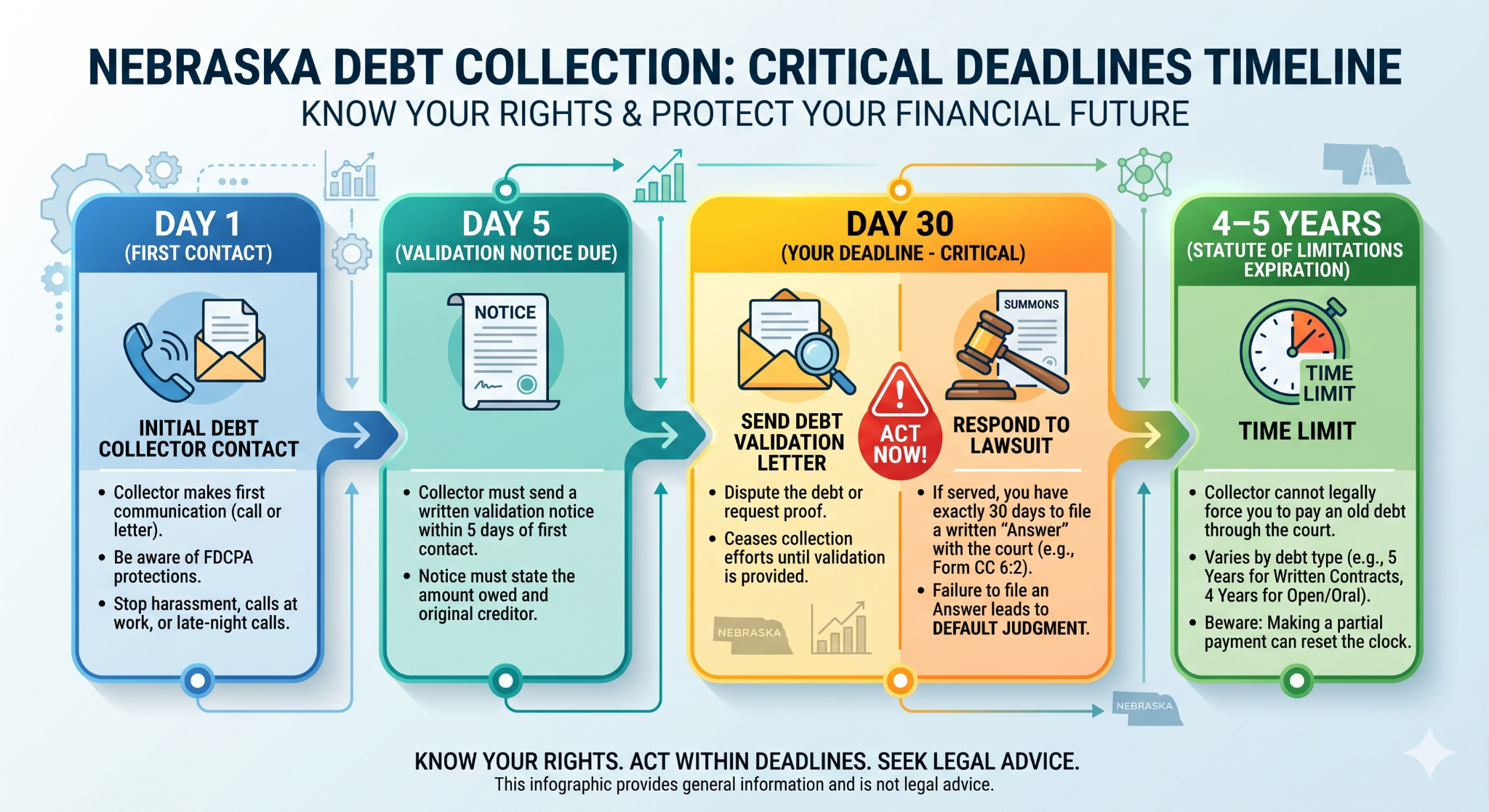

- You have exactly 30 days to respond to a lawsuit. If you do nothing, they win automatically.

- You can request debt validation in writing and dispute errors before making payment.

Thousands of Nebraskans deal with aggressive debt collectors every year. But you have legal rights, and they are stronger than most people realize. Nebraska debt collection laws set strict rules on what collectors can and cannot do. This article covers the specific protections, deadlines, and steps you can take.

Your Rights on Debt Collection and How to Use Them

You might feel like the debt collector holds all the cards, but that isn't true. Both federal law and Nebraska debt collection laws set strict boundaries on what a debt collector can and cannot do.

What debt collectors cannot legally do to you

The main law protecting you is the Fair Debt Collection Practices Act (FDCPA). It applies to third-party debt collectors, who are agencies hired to collect the debt. They are not the original creditor, such as the bank that gave you the loan.

As per the FDCPA, debt collectors absolutely cannot do:

- Call at inappropriate times: They are not allowed to call you before 8:00 AM or after 9:00 PM unless you told them it was okay.

- Call you at work: If you tell them verbally or in writing that your boss doesn't allow personal calls, they must stop calling your workplace immediately.

- Tell your neighbors: They can call others only to ask for your address or phone number. They cannot tell your boss, neighbor, or family member that you owe money.

- Lie to you: They cannot pretend to be police officers, lawyers, or government agents. They cannot claim you committed a crime.

- Threaten or abuse you: They cannot threaten violence, arrest, or property seizure if they don't actually have the legal right or intention to do it.

How to Stop Debt Collection Calls

When a debt collector calls, you don't need to argue. You just need to set boundaries.

If you want them to stop calling, you may use this script: 'I am recording this call for my records. Under the FDCPA, I am requesting that you cease all telephone communication with me immediately. If you have any information regarding this debt, send it to me in writing at my home address. Do not call my workplace or my home again '

Once you say this, hang up. You don't need to listen to their response. If they call again, they are breaking the law, and you might be able to sue them for damages.

Send the Debt Validation Letter

Never pay a single dollar until you are completely sure that the debt is yours, and the amount is correct. Debt collection laws in Nebraska and federal laws give you the right to 'validate' the debt.

Within five days of first contacting you, the debt collector must send you a written notice. This notice tells you how much you owe and who the original creditor was.

What should you do?

If something looks fishy, or if you just aren't sure, write a 'Debt Validation Letter' within 30 days.

Why do this?

Once they get your letter, they must stop trying to collect it until they send you proof (like a copy of the original bill).

Many debt buyers/debt collection agencies buy old debts without getting the original paperwork. If they can't find the documents, they often just give up and go away.

"The biggest mistake Nebraska consumers make is inadvertently resetting the legal clock. The moment you make a token payment, you hand the collector a fresh weapon. It revives their ability to sue you under Nebraska law, so you must demand written verification before ever opening your wallet.”

When Your Debt Is Too Old to Collect in Nebraska

One of the most important concepts to understand is the Nebraska statute of limitations. This is the legal 'expiration date' on a debt.

Once a debt passes this date, it is considered 'time-barred.' This means the debt collector cannot legally force you to pay. They can still ask you to pay, but if they sue you, you can get the case thrown out immediately.

The deadlines you need to know

The clock starts ticking from the date of your last payment or the last time you used the account.

| Type of Debt | Statute of Limitations | Primary Citation | Legal Notes |

|---|---|---|---|

| Written contracts (signed promissory notes, most personal loans, car loans, mortgages, etc.) | 5 years | Neb. Rev. Stat. § 25-205 | Correct, unchanged |

| Credit-card debt & revolving charge accounts | 5 years | Neb. Rev. Stat. § 25-205 | Credit card agreements are generally treated as written contracts under section 25-205 because they involve a signed or accepted written agreement. The 5-year statute of limitations applies. |

| True open accounts (medical bills, utility bills, unpaid invoices with no signed agreement) | 4 years | Neb. Rev. Stat. § 25-206 | Still 4 years, only applies when there is no written agreement at all |

| Oral / verbal agreements | 4 years | Neb. Rev. Stat. § 25-206 | Correct |

| Promissory Notes | 5 years | Neb. Rev. Stat. § 25-205 | Correct |

How to Avoid the Zombie Debt Trap

Debt collectors often buy old, expired debts for pennies on the dollar. They know they can't sue you, so they try to trick you into 'reviving' the debt. This is called a Zombie debt.

How the trap works: They call you and say, 'Look, just pay us $10 today to show good faith, and we will stop calling.'

The danger: In Nebraska, making a partial payment, even just $1, can reset the clock. If that 5-year limit had expired, your $1 payment starts a brand new 5-year clock. Suddenly, they can sue you again.

What to do: Never make a 'good faith' payment on an old debt until you have checked your credit report to see exactly when the 'Date of Last Activity' was. If it was more than 5 years ago, do not pay a cent without talking to a lawyer.

How to Handle Wage Garnishment

If a collector sues you and wins, they get a 'judgment.' This allows them to ask the court to take money directly from your paycheck. This is called wage garnishment.

However, Nebraska debt collection laws have specific protections to make sure you aren't left with nothing.

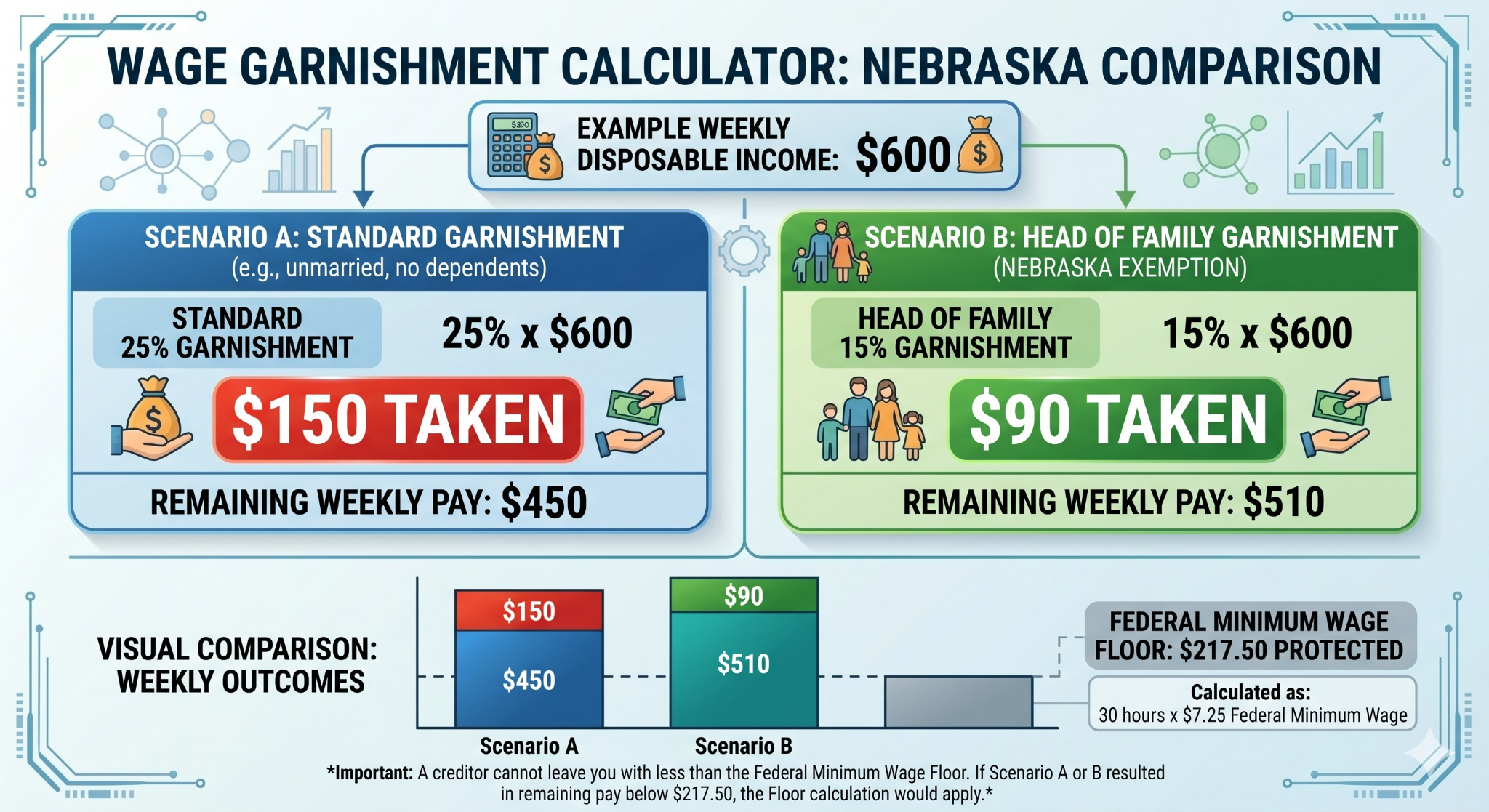

How the head of family exemption cuts garnishment to 15%

Most experts may tell you that creditors can take 25% of your disposable income for a week. While that is the federal standard, Nebraska offers a much better deal if you know how to ask for it.

The rule is: If you are the 'Head of a Family,' Nebraska law limits garnishment to just 15% of your disposable earnings.

You will qualify if you are a 'Head of a Family' and provide more than 50% of the support for a dependent (like a child, a spouse, or an elderly parent).

This doesn't happen automatically. You usually have to file an affidavit or claim this exemption with the court. If you stay silent, they will take the full 25%.

The minimum wage trap

Nebraska law also says that a creditor cannot leave you with less than 30 times the federal minimum wage per week.

Here is the problem:

- Federal Minimum Wage: $7.25/hour

- Nebraska Minimum Wage (2026): $15.00/hour

The protection floor is calculated using the federal number ($7.25 x 30 = $217.50/week). This is extremely low. Because Nebraska's actual minimum wage is $15.00, almost everyone earns more than the 'protected' amount.

You cannot rely on the minimum wage protection to save your paycheck. You must rely on the 15% Head of Family exemption or negotiate a payment plan before it gets to this stage.

How to Respond to a Lawsuit

Getting served with a lawsuit is scary. Your first instinct might be to hiding the papers in a place where none of your family can find them.

Do not do that.

If you ignore the lawsuit, the court assumes everything the collector said is true. They issue a Default Judgment. This gives them the power to legally seize your assets, such as through wage garnishment or bank account levies. All of these will happen because you didn't file a piece of paper. So, calm down and follow these steps. If you are facing an impending lawsuit, then you must explore Nebraska bankruptcy laws.

Step 1: Check the Date. You have 30 days from the day the papers were handed to you (or mailed to you) to file your response. Mark this on your calendar immediately.

Step 2: Get the Right Form. You don't need to write a legal essay from scratch. You need to file a formal 'Answer.' Contact the Clerk of the Court listed on your summons to find the correct form for filing an Answer in your county.

- Look for the Nebraska Court Form for answering a civil complaint in County Court (Form CC 6:2). You can download it from the Nebraska Judicial Branch website under the "Forms" section, specifically for County Courts.

- Direct Link Search: Search for "Nebraska County Court Answer Form CC 6:2" or look for "CC 6:2" in the Nebraska Judicial Branch civil forms repository.

- Alternative Pathway: Go to supremecourt.nebraska.gov > "Self-Help" > "Court Forms" > "County Court".

"Focus immediately on challenging their legal standing. You must force the debt buyer to prove they actually own your account. If you ignore this or submit a generic response, the creditor secures an easy default judgment, giving them full power to garnish your wages."

Step 3: Fill It Out. The form is simple. It asks you to respond to the claims.

- Deny: If you disagree with the amount, the fees, or who owns the debt, you check 'Deny.' This forces them to prove their case in court.

- Affirmative Defenses: This is where you tell the judge why you shouldn't pay.

- Example: 'The debt is past the Nebraska statute of limitations.'

- Example: 'I am a victim of identity theft.'

- Example: 'The amount includes illegal fees not in the original contract.'

Step 4: File It. Take the original Form to the Clerk of the Court listed on the summons. Mail a copy to the collector's lawyer. Ask the clerk for a stamped copy for your own records.

Nebraska Debt Laws That Most People Miss

There are a few special rules in debt collection laws in Nebraska that might help your specific situation.

Hurt at work? Your medical debt collection may have to wait

If your debt is related to a medical injury that happened at work, and you have a Workers' Compensation case pending, tell the debt collector immediately.

Under Nebraska law (Neb. Rev. Stat. § 48-148.02), medical providers and debt collectors often have to 'stay' debt collection efforts on those specific bills. They must wait until the Workers' Comp court decides who is responsible for paying them.

Why you cannot go to jail for unpaid debt in Nebraska

Collectors sometimes imply that you could go to jail for unpaid bills. This is a lie. Nebraska abolished debtors' prisons long ago.

The exception - Civil Contempt: The only way you end up in jail is if you ignore a direct court order.

If the court orders you to fill out a 'Debtor's Exam' listing your assets, and you refuse to do it, the judge can hold you in 'Contempt of Court.' You are going to jail for defying the judge, not for owing money. So, never ignore a court order to appear or answer questions.

How to Protect Your Bank Account from a Levy

If a collector wins a judgment against you, they can ask the court to freeze your bank account and take money directly from it. This is called a bank levy or bank garnishment.

However, not all money in your account can be taken. Under federal and Nebraska law, certain funds are protected:

Federally Protected Funds:

- Social Security benefits

- Supplemental Security Income (SSI)

- Veterans' benefits

- Federal student aid

- Railroad retirement benefits

How the Protection Works:

If your bank receives a garnishment order, it must review the last two months of deposits to check for protected federal benefits. If protected funds are found, the bank must automatically protect up to two months' worth of those benefits from the levy. You do not need to do anything for this automatic protection to apply.

What You Should Do:

If your account contains only exempt funds like Social Security, file a claim of exemption with the court immediately. Ask the bank for help if you are at risk of a judgment. If a debt collector threatens to freeze your bank account, talk to a debt specialist before the levy is filed. There may be options to negotiate a payment plan and avoid a freeze entirely.

How to Dispute a Collection on Your Credit Report

Under the Fair Credit Reporting Act (FCRA), which works alongside Nebraska debt collection laws, you have the right to dispute any inaccurate collection entry on your credit report.

When to Dispute:

- The debt is not yours (wrong person or identity theft)

- The amount is wrong

- The account has already been paid or settled

- The debt is past the 7-year credit reporting limit

- The collection was reported before the required waiting period

How to File a Dispute:

- Get your free credit report from AnnualCreditReport.com.

- Identify the collection entry you want to dispute.

- Write a dispute letter to the credit bureau (Equifax, Experian, or TransUnion) explaining why the entry is inaccurate.

- Include copies of any supporting documents (payment receipts, validation letters, court records).

- Send the letter by certified mail with return receipt requested.

The credit bureau has 30 days to investigate and respond. If the bureau cannot verify the debt, they must remove it from your report. Under the FCRA, collection accounts can stay on your credit report for up to seven years from the date of your first missed payment.

Original Creditor vs. Debt Collector vs. Debt Buyer - Know the Difference

The entity contacting you about your debt matters. Different rules and leverage apply depending on who is trying to collect.

| Original Creditor | Third-Party Debt Collector | Debt Buyer | |

|---|---|---|---|

| Who are they? | The company that gave you the loan or credit card (your bank, hospital, etc.) | An agency hired by the creditor to collect on their behalf | A company that purchased your debt, usually for pennies on the dollar |

| Does the FDCPA apply? | Generally no, the FDCPA applies only to third-party collectors | Yes, full FDCPA protections apply | Yes, full FDCPA protections apply |

| Do they have original documents? | Yes, they have all the original paperwork | Sometimes, they may have copies from the creditor | Often no, many debt buyers lack the original signed agreement |

| Your leverage | Lower, they have all the proof | Medium, you can demand validation and challenge their authority | Highest, many debt buyers cannot prove the debt if challenged |

| Negotiation range | May offer hardship plans or payment arrangements | Typically authorized to settle for a percentage | Most willing to settle for 30–40% because they bought the debt cheaply |

| Nebraska statute of limitations | Same 5-year or 4-year limits apply | Same limits apply | Same limits apply, but the clock does NOT restart just because the debt was sold to a new buyer |

If a debt buyer sues you under Nebraska debt collection laws and cannot produce the original signed agreement, you may be able to get the case dismissed by challenging their standing in your Answer.

How to Negotiate With The Debt Collector Like a Pro

If you know you owe the debt but can't pay the full amount, you can negotiate. Debt collectors often prefer a quick debt settlement in Nebraska over a long court battle.

- Lump Sum Settlement: If you have some cash (from a tax refund or sale of an item), offer them 30-40% of the total debt to settle it 'in full'. Get the agreement in writing before you pay.

- Hardship Plan: If you have no assets and a low income, tell them. Collectors call this being 'judgment proof'. If they know they can't garnish you (because you are on Social Security or unemployment), they might stop calling.

- Pay for Delete: Under federal law, a collection account can stay on your credit report for up to seven years. So, ask them to remove the negative mark from your credit report in exchange for payment. They don't have to do this, but some will agree to it to get paid.

Frequently Asked Questions (FAQ)

For most written contracts, like credit cards and personal loans, the Nebraska statute of limitations is five years. This clock starts ticking from the date of your last payment or activity. Be careful: if you make even a small 'good faith' payment on an old debt, you can accidentally restart this five-year clock, giving the collector a fresh chance to sue you.

Under Nebraska debt collection laws, a creditor can typically garnish up to 25% of your disposable earnings. However, if you are the 'Head of a Family' (meaning you support dependents), you can file an objection to lower that cap to just 15%. This is a specific Nebraska protection that many people miss because they don't know to ask for it.

They cannot just show up and take your property. First, they must sue you and win a judgment. Even then, debt collection laws Nebraska offers exemptions. For example, the 'Homestead Exemption' (Neb. Rev. Stat. § 40-101) protects up to $120,000 of equity in your home, and there are specific exemptions for your car (up to a certain value) and tools of your trade.

Yes. Under the federal FDCPA, which works alongside Nebraska debt collection laws, if you send a written letter telling a collector to stop contacting you, they must comply. Once they receive it, they can only contact you to confirm they are stopping or to notify you of a specific legal action, like a lawsuit.

You have 30 days from the date you receive the Summons and Complaint to file a written Answer with the court. Do not ignore it. If you do nothing, the court will enter a default judgment against you, which gives the collector the right to garnish your wages and freeze your bank account. You can download the Answer form from the Nebraska Judicial Branch website and file it with the Clerk of the Court listed on your summons.

Looking For An Effective Debt Relief Option?

Attorney Lyle Solomon and the team at Oak View Law Group have helped more than 7,600 people successfully resolve their outstanding debt issues. The consultation is completely free, and there is absolutely no obligation to move forward until you are ready.

Request a Free Consultation | Take the Debt Relief Suitability Assessment | Call (800) 530-OVLG

Bottom Line

Nebraska debt collection laws give you real protections, but only if you use them. Remember these critical deadlines: You have 30 days to respond to a lawsuit or the collector wins by default. You have 30 days to send a debt validation letter after first contact. The statute of limitations is 5 years for written contracts and 4 years for open accounts. If the debt is older, you may be able to get the case dismissed. If you qualify as Head of Family, you can cut wage garnishment from 25% to just 15%.

Whether you are mailing a cease and desist letter, checking the statute of limitations on an old medical bill, or filing an Answer in court to protect yourself from wage garnishment, you are back in control. If you're managing multiple unsecured accounts, be sure to check the debt consolidation option once, if possible. For issues with aggressive short-term payday lending, you can explore your options in Nebraska payday loan laws.

Sources

- Nebraska Judicial Branch - Self-Help Forms: Download the official 'Answer forms and instructions to represent yourself in court.

- Nebraska Attorney General - Consumer Protection: File a formal complaint here if a debt collector is harassing you, lying, or breaking FDCPA rules.

- Consumer Financial Protection Bureau (CFPB) - Submit a Complaint: Submit a complaint to this federal agency to get help resolving issues with large collection agencies.

- Nebraska Revised Statute § 25-205: Read the official state law establishing the five-year statute of limitations for written contracts.

- Mass.gov Guide to 'Zombie Debt': Understand how debt collectors try to trick you into restarting the clock on expired debts.

- U.S. Department of Labor - Wage Garnishment Fact Sheet: Review the federal rules and limits regarding exactly how much of your paycheck can be garnished.

- Nebraska Revised Statute § 25-1558: Read the Nebraska law detailing state wage garnishment limits and specific income exemptions.

- U.S. Department of Labor - Minimum Wage: Check the current federal minimum wage used as the baseline for calculating garnishment limits.

- Nebraska Department of Labor - Minimum Wage: Check the official Nebraska state minimum wage updates that directly affect your paycheck protections.

- Cornell Law Institute - Default Judgment (Rule 55): Learn what a default judgment is and why you must never ignore a court summons.

- Nebraska Revised Statute § 48-148.02: Read the law that pauses debt collection efforts while your workers' compensation case is pending.

Disclaimer: This article provides general information about debt collection laws in Nebraska for educational purposes only, and it should not be construed as legal advice. If you are facing debt collection actions, consider consulting with a qualified attorney who can review your specific circumstances. Oak View Law Group provides debt relief services and offers free consultations to help you understand your options. Service fees apply to enrolled programs. Individual results vary based on debt amount, creditor cooperation, and financial circumstances. See OVLG's refund policy for details.